UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

|

| |

Filed by the Registrant S | Filed by a Party other than the Registrant £ |

Check the appropriate box: | |

|

| |

£ | Preliminary Proxy Statement |

£ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

S | Definitive Proxy Statement |

£ | Definitive Additional Materials |

£ | Soliciting Material Pursuant to §240.14a-12 |

|

|

FULL HOUSE RESORTS, INC. |

(Name of Registrant as Specified In Its Charter) |

|

(Name of Person(s) Filing Proxy Statement, if other than the Registrant) |

Payment of Filing Fee (Check the appropriate box):

|

| | |

S | No fee required. |

£ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

| (1) | Title of each class of securities to which the transaction applies: |

| | |

| (2) | Aggregate number of securities to which the transaction applies: |

| | |

| (3) | Per unit price or other underlying value of the transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

| | |

| (4) | Proposed maximum aggregate value of the transaction: |

| | |

| (5) | Total fee paid: |

| | |

£ | Fee paid previously with preliminary materials. |

£ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| (1) | Amount Previously Paid: |

| | |

| (2) | Form, Schedule or Registration Statement No.: |

| | |

| (3) | Filing Party: |

| | |

| (4) | Date Filed: |

| | |

Dear Fellow Shareholders:

This was the third year of our company's new management team, and we made great progress in strengthening the company and moving it towards a prosperous future.

In our first year, we stabilized results, which had been declining at virtually every property, and completed the challenging construction of the hotel at our Mississippi property. In our second year, we announced plans for improvements at each property; completed a rights offering to partially fund those improvements; and acquired Bronco Billy's Casino and Hotel in Cripple Creek, Colorado, our second-most-important property. In our third year, we began to implement those numerous improvements at our existing properties while we developed an ambitious plan to expand Bronco Billy's. At the same time, we continued to explore the possibility of relocating part of our underutilized gaming capacity within Indiana. More recently, we refinanced all of our debt, extending maturities and reducing its cost. We then completed a direct placement of equity to help fund the first phase of the Bronco Billy's expansion.

Since we joined the company, our stock price has approximately tripled. We can't promise that it will triple again in the next three years, but we will continue to work hard to provide good returns for our shareholders, to create great experiences for our guests, and to be good employers for our team.

The Year

Sometimes, I wish a year had only nine months. The first nine months of 2017 were excellent. Compared to 2016, our net revenues grew 24%, 16% and 6% in the first, second, and third quarters of 2017, respectively. Every property showed improvement in the nine-month period.

Results in the fourth quarter were not as good. As it happens every few years, a hurricane passed through the Mississippi Gulf Coast. It did little property damage but affected our business for approximately a week, including a key weekend when we were forced to close. That hurricane period corresponded with one of the region's most important promotions, "Cruisin' the Coast," necessitating the cancellation of the promotion. Mother Nature also was not kind to us in Indiana, where an ice storm hurt the important New Year's Eve holiday, and at Lake Tahoe, Nevada, where a dearth of snow affected the important ski season.

The poor weather continued in January and February, with flooding on the Ohio River causing us to close Rising Star for several days and still no snow at Lake Tahoe. Then, suddenly, the weather returned to relatively normal conditions in March, with lots of snow at Lake Tahoe and sunshine on the Mississippi Gulf Coast. As our weather returned to normal, so did strong business levels.

We are fairly diverse for a small company, but not diverse enough that we can rely on good weather at some properties to always offset bad weather at others. If two or three of our properties are affected by poor weather, it is difficult for the others to pick up the slack. On the other hand, there are periods like March where all five of our properties appeared to perform well.

Despite the weak fourth quarter, net revenues grew 11% in 2017 versus 2016, net loss improved to a net loss of $5.0 million from a net loss of $5.1 million, and Adjusted EBITDA1 rose 2%. Much of that growth was attributable to a full year of ownership of Bronco Billy's, which we acquired in May 2016. Also, because of our large depreciation and amortization charges, we generally produce positive cash flows from operations despite net losses. In fact, our cash flow from operations was $7.1 million in 2017, versus $7.9 million in 2016.

__________

1 Please see the endnote to this letter for a discussion of non-GAAP measures such as Adjusted Property EBITDA.

Silver Slipper Casino and Hotel

The Silver Slipper is still our most important property, generating 51% of our Adjusted Property EBITDA in 2017. Its Adjusted Property EBITDA was $10.7 million for the year, versus $10.0 million in 2016.

Gaming revenues at this property rose 7% for the year, versus only 0.3% growth for the Mississippi Gulf Coast casinos as a group. Its results also compared favorably with the 4% increase in gaming revenues shown by the four casinos in the New Orleans metropolitan area, with which it also competes.

We made several improvements at the Silver Slipper during the year. First, in June 2017, we opened the popular Bayou Caddy Oyster Bar, the first new food and beverage outlet at the casino since it opened in 2006.

In August 2017, we opened the Silver Slipper Beach Club. Yes, one generally prefers to open a beach club at the beginning of the summer rather than at the end, but we ran into some construction challenges. The good news is that it looks great. It recently reopened after the winter and will remain open for the entire 2018 summer season.

It's also much more than just a "beach club." It offers an infinity-edge pool overlooking the beach, the only such pool on the Mississippi Gulf Coast. The pool adjoins an attractive bar and a pool deck, surrounded with 23 majestic Zahidi palm trees imported from California. The entire beachfront complex fronts our hotel, making a much more impressive "sense of arrival" than it had previously.

We've also started planning a potential expansion of the Silver Slipper. We lease approximately 38 acres of land, with a purchase option beginning in February 2019. We utilize only approximately 7 of those acres, but much of the remainder is wetlands. There is also an abandoned pier in front of our property. The pier, including the underlying bottomlands, is owned by the State of Mississippi.

We compete with numerous casinos in southern Mississippi and Louisiana. We think this is a mature market, with casinos having operated in the region for more than 25 years. There is no limit on the number of casinos that can be built in the state of Mississippi, but we think that the economics would be challenging to build a new casino. Indeed, a casino with an investment of approximately $290 million opened in Biloxi in December 2015 and appears to be generating a sub-par return on its investment. The Silver Slipper itself cost $70 million when it was originally built in 2006. Different improvements have been made in the interim, including a $21 million hotel addition in 2015. Hence, its replacement cost today is probably between $125 million and $150 million and its income relative to that replacement cost is not scintillating. (Its replacement cost is also not what is reflected in our share price, as stocks tend to reflect earnings and potential of the assets, rather than replacement costs.) While there always seems to be someone trying to add a new casino in the region, we think the economics do not work well and that we are relatively protected from that competitive threat.

On the other hand, we do think it can make sense to add to an existing property. One of our competitors is currently expanding its casino capacity, which we think is curious as its existing large casino doesn't seem to be operating with capacity constraints. One of the most common misconceptions in the gaming industry is that a casino's revenues are a function of the number of slot machines. At some point, of course, that could be true; for most casinos, though, it isn't. Slot machines don't gamble; people do. Casino revenues go up when there are more people.

The hotel that we opened in 2015 operated at 88% occupancy in 2017. Granted, much of that occupancy was from rooms that we provided free or at reduced rates to casino customers, but, frankly, we don't care if our guests pay for their overnight stay at the front desk or at our slot machines. The hotel clearly brings more people to our casino, and our hotel guests tend to stay longer and gamble more than people who are not staying overnight.

We think the numbers work to add an additional hotel to the property. Along with that, we would need to add some meeting room space to help fill the hotel mid-week and during the slower seasons. We would also need additional parking to accommodate the additional guests.

The best place to build a new hotel tower is over the abandoned pier in the gulf. The guest rooms would then be conveniently located near our casino and also have stellar views along our white-sand beach on one side and, on the other side, of the picturesque fishing boats cruising up the adjacent channel.

All of this is doable, but complicated. We have prepared a master plan for the potential hotel, meeting room space and additional parking. We have begun the process for leasing bottomlands and seeking other approvals from the State of Mississippi. The plan will also require permits from certain environmental agencies and the Army Corps of Engineers. Combined, this is a lengthy process, probably requiring years, and there is no certainty that we will obtain all of the necessary approvals. However, an opportunity never pursued will never see fruition. So, we have begun.

Bronco Billy's Casino and Hotel

Our plans for Bronco Billy's are much more immediate.

We acquired Bronco Billy's in May 2016 at a purchase price of $31.1 million. It earned $4.8 million of Adjusted Property EBITDA in 2017, reasonably close to the $5 million per year that it averaged in past years and in line with our expectations.

During 2017, however, we realized that Cripple Creek offers a bigger opportunity than we had originally thought.

Colorado is a large state. Its west half is dominated by the Rocky Mountains, while its eastern half consists of farms and ranches of the Great Plains. Ninety percent of the state's population of 5.6 million lives at the interface between the two ó the so-called "Front Range," consisting of Denver and related communities in the north and, an hour south of that, Colorado Springs and the smaller cities of Pueblo and CaÒon City. The Northern Front Range has almost 4 million residents. The Southern Front Range has almost a million residents. Both are growing rapidly.

Gold and valuable minerals were discovered in the Colorado Rockies in the 1800s and the state's history is closely related to those mining communities. Denver and Colorado Springs were largely built using the profits from the state's gold mines. The mining communities were high up in the mountains, where thousands of hard-working miners toiled in search of their fortunes. Over time, many mines were exhausted of their gold and minerals. Meanwhile, mining techniques changed. Today, small amounts of ore and minerals can be efficiently removed from large amounts of dirt, using large earth-moving equipment rather than legions of individual miners. The result was a series of mining towns in the mountains of Colorado that were no longer needed to house and supply large numbers of miners. A few of those towns built ski areas and golf courses and morphed into famous destination resorts, including Aspen, Telluride and Breckenridge.

Three of the largest of these towns didn't have either the topography or the snowfall to host major ski resorts. Those three towns ó Cripple Creek, Black Hawk and Central City ó endured declining populations for a century. Cripple Creek itself had a population of approximately 10,000 people in 1900 and it was the commercial center of a mining district with some 35,000 people. By 1990, Cripple Creek's population had declined by 95% to only about 500 hardy souls.

Colorado legalized casino gaming in 1991 in Cripple Creek, Black Hawk and Central City in order to prevent them from becoming ghost towns. Black Hawk and Central City, located approximately an hour west of Denver, abut each other. Cripple Creek is approximately one hour west of Colorado Springs. As Denver and Colorado Springs are approximately an hour apart, Cripple Creek is approximately two hours from Denver and Black Hawk/Central City is approximately two hours from Colorado Springs. There are also two tribal casinos in the state, located on reservations in the remote southwestern "Four Corners" region. There are no Native American reservations in the Denver/Colorado Springs area.

Originally, gaming in Colorado was limited to a maximum bet of $5. That tended to make it a low-brow, slots-oriented activity. At $5 per hand, the casinos could not afford to build the luxury hotels, high-end restaurants and spas that are common to casinos in other markets. The low stakes also did not appeal to wealthier clientele, accustomed to more exciting gaming activity in Las Vegas and elsewhere.

This changed in 2009, when the state raised the betting limit twenty-fold to $100 per hand. At $100 per hand, Colorado gaming becomes appealing to a much broader range of customer. It also becomes economical to offer higher-end hotels and restaurants.

Operators in Black Hawk responded to the regulatory change, building new hotels and other facilities. Black Hawk's revenues grew, while those of Cripple Creek stagnated and even showed a slight decline. We know from our own focus groups that some potential customers from Colorado Springs choose to gamble in Black Hawk precisely because of those hotels and other facilities, even though Black Hawk is twice as far as Cripple Creek. Based on the relative populations of the North and South Front Range statistical areas, one would expect the revenues of Black Hawk/Central City to be four times those of Cripple Creek. Instead, they are five times as much. Table games revenues are eight times. EBITDA, as reported by the gaming commission, is nine times.

Yet, this isn't just a market share game between Black Hawk and Cripple Creek. Denver and Colorado Springs are among the fastest-growing cities in the country, with companies and residents attracted by the climate, the accessibility of the mountains, the central U.S. location, a business-friendly government and a high quality of life. The population of the Colorado Springs metropolitan area, for example, has grown by approximately 13% since the last new casino opened in Cripple Creek, some 10 years ago. From 2010 to 2016, the population of the Denver MSA grew by approximately the population of Reno, Nevada's second-largest city. And there are no signs of that growth slowing any time soon.

Moreover, Colorado is a strongly underpenetrated market. Total U.S. gaming revenues in 2016 are estimated at $65 billion, or about $201 per capita. That includes states like Hawaii and Utah, which have no casinos. Cities like Baton Rouge, Kansas City

and Cincinnati have gaming spend per capita of approximately $300 to $400. Gaming spend per capita in the Northern Front Range is approximately $174, while that in the Southern Front Range is only approximately $148.

Perhaps the most comparable market is Washington. Like Colorado, Washington is geographically a large state, with most of its population of 7.4 million concentrated in one extended metropolitan area ó the Seattle-Tacoma-Olympia combined statistical area. According to the Washington State Gambling Commission, the total gaming revenues in the state are approximately $2.7 billion per year. Most of that is from the state's 28 tribal casinos. Those casinos are required to be on reservation land, which is generally located in rural areas some distance from the population centers. As in Colorado, most people in Washington have to drive some distance to visit a casino. Yet, the current gaming revenues per capita in Washington is approximately double that of Colorado. We know of no inherent reason why this should be the case, except that the tribal casinos in Washington often offer hotels, quality restaurants, entertainment and other amenities. Only one casino in Colorado offers the scale and breadth of amenities of most of the Washington tribal casinos ó the highly successful Ameristar casino in Black Hawk.

Therein lies our opportunity. Cripple Creek today is primarily a day-trip destination. Based on its gaming revenues as reported by the Colorado Gaming Commission and the win per visitor at Bronco Billy's, we estimate that Cripple Creek receives approximately 1.5 million visitors per year. We further estimate that only about 10% of those visitors stay overnight. The entire town has only approximately 450 hotel rooms. Of these, more than one-third are at one hotel, with small guest rooms built in the 1990s designed to accommodate customers under that $5 gaming limit. Many of the rest are "bed and breakfasts," some of which are quite nice and others of which are less appealing.

It creates an unusual phenomenon in our casino. At most casinos, business peaks in the late evening as gamblers finish dinner and retire to the casino for their entertainment. In Cripple Creek, many of the visitors don't even stay for dinner. They head home, seeking to get down from the back side of Pike's Peak before dark. The casinos are oddly quiet in the late evening. Furthermore, because of the short stays, very few visitors participate in activities other than gaming. At one time, Bennett Avenue had dozens of gift shops. Today, it has about a half a dozen. The local theater, The Butte, provides quality productions, but can only exist with substantial town subsidies. Midweek, it is sometimes difficult to find a restaurant that bothers to stay open for dinner.

We can change this. We've held focus groups in Colorado Springs and we know that there is ample demand for a high-quality hotel experience in Cripple Creek. We also know that there are meetings and conventions that can be lured to this unique historical venue. Indeed, the Broadmoor Hotel in Colorado Springs (built, incidentally, with profits from the Cripple Creek gold mines) is one of the largest five-star hotels in the U.S. It has a very important national and international convention and meeting business. Most of our customers are likely to come from Colorado Springs itself, but perhaps some of those convention attendees in Colorado Springs would extend their stays and come up the mountain before or after their convention.

So over this past year, we acquired land and options on land behind and adjoining Bronco Billy's. We then designed a four-star hotel that can be built on this land with substantial meeting room space, a spa, a heated outdoor swimming pool, and a gourmet restaurant. This will occupy much of the casino's existing surface parking lots, so we designed a convenient parking garage directly connected to the casino. To integrate this new hotel with our existing casino, much of which was built in the 1890s, we are refurbishing a significant portion of our property.

This is a unique place. Substantially all of Cripple Creek is a historical district with strict architectural codes. We had to design the hotel carefully to blend into and complement the neighborhood, without having new buildings that simply mimic the authentic historic buildings that surround us. To build our hotel and tie together the complex, we are also seeking to vacate a street and a portion of an alley that run through our property, as well as some other minor variances. Our plans were recently endorsed unanimously by the city's Historical Preservation Committee and we expect the required entitlements to be considered by the Cripple Creek City Council within the next few weeks.

We intend to operate our casino throughout the construction period. It makes money. Equally important, it accommodates our customers (many of whom are regular visitors) and employs our staff. We need to build the parking garage first, as otherwise we would not have parking available for our guests during construction. If all goes well, we hope to break ground on that parking garage in the second quarter and complete it around year-end. Then, we would start construction on the hotel itself in the first part of 2019 and open it in 2020.

We recently raised approximately $11.8 million through a direct equity placement. We intend to use that money to help build the parking garage, while we arrange the broader financing for the larger second phase. Note that the parking garage itself should be a major "plus" for Bronco Billy's. Several of our major competitors offer parking garages. In this mountain environment, rain and snow are not uncommon. At those times, a parking garage can be an important competitive amenity.

As we assembled our site, we also obtained options on attractive terms to acquire the Imperial Hotel and to either acquire or lease the Imperial Casino. The Imperial Hotel is a historic structure that has been largely refurbished in recent years. It offers 12

refurbished guest rooms, another four rooms in various stages of refurbishment, a restaurant, a meeting room, and a 150-seat theater. It is connected to the Imperial Casino, which sits on a key corner of Bennett Avenue and Third Street and has been closed for the past few years. We think we can operate it profitably as a satellite of our Bronco Billy's operation, earning a nice return on a modest investment while providing some diversity within the Bronco Billy's complex. The Imperial Hotel has been operating seasonally. We intend to complete the refurbishment of the hotel, add an elevator, and operate it year-round. The Imperial Hotel and Casino should also benefit from the nearby Bronco Billy's parking garage.

Rising Star Casino Resort

Our largest casino, in terms of footprint, is Rising Star in Indiana, near Cincinnati. It has two hotels totaling 294 guest rooms, an 18-hole golf course, several restaurants, a ballroom that can also host entertainment events, and a casino offering 917 slot machines and 25 table games. We added a 56-space RV Park to the property in August 2017.

Rising Star opened in 1996 and was the first casino in the region that includes Cincinnati (population of 1.6 million, approximately 45 minutes away), Louisville (1.0 million, 90 minutes away) and Indianapolis (2.0 million, two hours away). For several years, this casino produced roughly $50 million per year in EBITDA ó over twice the Adjusted EBITDA of our entire company today.

Rising Star's most important market is the Cincinnati metropolitan area, which spills over into Northern Kentucky. It sits along the west side of the Ohio River and, unfortunately, there is no bridge at this location. The closest bridges are approximately 20 miles to the north and south of Rising Sun. After Rising Star's opening, other casinos opened on the Indiana side of each of those bridges. Most of Rising Star's customers must drive several miles past a competing casino before arriving at Rising Star. Then, Ohio legalized a limited number of casinos, with several opening in the Cincinnati metropolitan area about five years ago. Now, Rising Star is the oldest and most geographically challenged casino in the region.

We're about to change that. We've spent the past few years acquiring land and various permits to operate an interstate car ferry service from our property to Northern Kentucky. The river is only approximately 2,100 feet wide, but it requires almost an hour to drive from our property to the town directly across from us. Inland from that Kentucky town is the Cincinnati/Northern Kentucky International Airport, which has attracted numerous businesses and residential developments around it. The population on the Kentucky side of the river is significantly higher and growing faster than the population in the Indiana side. The ferry service will make Rising Star much more convenient to a much larger population base.

The ferry boat consists of a barge with landing ramps and a tugboat that pushes it back and forth across the river. We've had both built to our specifications and they will be ready to go within a few weeks. Meanwhile, we've obtained permission from a myriad of agencies to begin construction on the roads and ramps on both sides of the river. We are moving as quickly as weather will allow and hope to have this construction completed in July.

Our permits allow us to carry 10 vehicles on each crossing. We estimate that the ferry can make approximately four round trips per hour. Ferries aren't very fast, but it also isn't very far. We plan to charge $5 per car, but will readily refund this fare with "free play" for customers who visit our casino.

We think we will be the first casino in history to operate a vehicular ferry. It's a bit of a guess as to how it will affect our casino, particularly since there are bridge alternatives. However, with almost any set of assumptions, it is likely to be a "plus" and could be a big "plus."

At the same time, we are sprucing up the property. Refurbishment of our main hotel lobby and the guest room corridors is under way and we start construction shortly on refurbishment of the central pavilion, which is the arrival route to the casino and the front door to our restaurants. It is the pavilion's first refurbishment since it opened some 22 years ago. We also plan to refurbish the casino, adding a VIP area later this year.

This year should also benefit from a full season of the new RV Park, which opened too late in the summer last year to have been much effect on our earnings in 2017.

All of these modifications are relatively modest in cost, but potentially major in impact. This property will probably never again earn the $50 million of Adjusted Property EBITDA per year that it earned in the 1990s, or even the approximately $10 million per year that it was earning before the casinos opened in Ohio. However, we think it can earn much more than the $2.7 million of Adjusted Property EBITDA that it produced in 2017, resulting in a high return on our reinvestment dollars.

Stockman's Casino

Stockman's is the largest and most complete casino in the small community of Fallon, Nevada, located approximately one hour east of Reno. Fallon is primarily an agricultural community, as well as home to the Navy's principal flight training school, popularly known as "Top Gun." It is also relatively close to the new Tahoe Reno Industrial Center, anchored by the large Tesla battery plant.

We've substantially improved the appearance of Stockman's over the past year. We demolished an administrative office building that blocked the view of our casino. We replaced that with a convenient surface parking lot, landscaped and lighted, with new entrances into the casino. We rebuilt the large marquee sign, adding the largest reader board in town. We repainted the coffee shop and improved its flooring. We also put a new roof on the casino and replaced a swamp cooler in the kitchen with air conditioning.

Revenues at Stockman's have increased in 10 of the past 12 months, as the improvements came online. We think this trend will continue over the year ahead, as some of those improvements were only recently completed.

Grand Lodge Casino

We operate the casino in the Hyatt Regency Lake Tahoe, one of the finest resort hotels in Northern Nevada. We lease the casino from the Hyatt Organization. That lease was scheduled to expire at the end of August 2018. In 2016, we reached an agreement with Hyatt to extend the lease and refurbish the casino. We committed to invest up to $1.5 million in slot machines, gaming tables, gaming chairs and other casino equipment and Hyatt committed to invest up to $3.5 million in other improvements to the casino space, including a much nicer casino bar operated by Hyatt. The agreement also extended the term of the lease by five years, to August 2023, with an increased rent from $1.5 million to $2.0 million per year.

The refurbishment was planned during 2016 and implemented in the first half of 2017. The construction disrupted our business during those months, offsetting some of the benefits of a strong ski season.

The refurbished casino opened just before the key summer season, but then we ran into a different challenge, one demonstrating the perils of operating a casino in a hotel owned by others. Hyatt, like many hotel companies, has implemented a policy of charging for parking.

We understand why Hyatt and other travel-related companies are doing this. As online booking sites and other technologies affect the hospitality industry, hotels have tended to hold the line on room rates, but have begun charging resort fees, parking fees, and a wide range of other separate fees. Generally, those fees are not shared with the online travel agencies.

Hyatt has been good at working with us, allowing us to "comp" the parking fees for our casino customers. There's also a local aspect to this, as there is not a large amount of parking in Incline Village and it was not uncommon for people to park in the Hyatt lots and go to the nearby beach. Nevertheless, the parking system and the hassle of having a parking ticket stamped is a deterrent. There are two other casinos approximately 5 miles away that are not as nice as ours but have ample free parking. Someone living in or visiting Incline Village might be going out to dinner and might now think twice about eating at the Hyatt's restaurants versus its competition, and some of those Hyatt restaurant customers would typically wander into our casino.

The parking fees appear to have offset at least some of the benefit of our refurbished casino. Our revenues last summer were similar to those of the preceding summer despite having a much nicer casino.

Then, there was no snow. The Hyatt has two seasons ñ the key summer months and the secondary ski season. Last year's ski season was great, sometimes with so much snow that the roads were closed. The most recent ski season started out very slowly. Over the Christmas holidays, the local ski resorts had only a few trails open, utilizing a great deal of snow-making equipment. By the end of February, the snowpack was only 29% of normal.

In March, it snowed. In fact, it snowed a lot, with the snowpack at the end of March reaching 78% of normal. Our casino also did quite well in March, but it is difficult to make up in one month the weakness in the business in December, January and February.

Looking ahead, our casino is in great shape, as is the Hyatt. We are hoping that our customers will eventually realize that the parking restrictions have positive aspects as well. The parking fees reduce the beachgoer usage and make more spaces available for casino customers, and we readily "comp" the fees for those customers.

Balance Sheet

We reinvested approximately $11.1 million into the company during 2017. This included the RV Park, a storage building for Christmas Casino decorations, the ferry boat, and entitlement work for the ferry roads and ramps at Rising Star; the Beach Club and Oyster Bar at Silver Slipper; the Crippled Cow bar and coffee outlet at Bronco Billy's; our portion of the refurbishment at Grand Lodge Casino; and much of the cost of the new parking and entrances at Stockman's. It also includes investments in new slot machines and related equipment, company-wide.

We generated approximately $7.1 million in free cash flow from operations. Our total debt was $96.1 million at the end of 2017, versus $98.3 million at the beginning of the year. Our total cash and equivalents, including cash used in operations, was $19.9 million at year-end and $27.0 million at the beginning of the year. Our net debt increased by $4.9 million during the year, indicating that more than half of our capital expenditures were funded from internal cash flows, with the remainder essentially funded by the rights offering that we completed in November 2016.

In February 2018, we refinanced essentially all of our long-term debt, decreasing the cost of that debt, extending the maturities, and reducing the interim amortization of debt. The cost of that new debt is LIBOR plus 7 percentage points, with a LIBOR floor of 1.0%. With LIBOR currently at 2.3%, the interest rate on the debt is now 9.3%. That compares with an average interest rate on our prior first- and second-lien debt of 10.5% at current LIBOR rates. We recently purchased an interest rate cap on an amount equal to half that debt, reducing our exposure to rising interest rates.

Then, in March 2018, we directly placed 3.9 million shares of stock at $3.00 per share, raising approximately $11.8 million from an assortment of institutions and qualified individuals. We had been approached by several investors over time who indicated that they wished to invest in our company, but that the trading volumes tend to be so modest that it was difficult to accumulate a significant position. Using our shelf registration, which was approved by the SEC in January, we were allowed to directly place the stock, rather than incur the significantly higher fees of an underwritten public offering.

It is our intent to use such additional funds to start construction as soon as possible on the first phase of the Cripple Creek expansion. That involves exercising certain real estate options that we have, building a parking garage attached into the existing casino at Bronco Billy's, and reopening the Imperial Hotel and Casino. We believe that we will receive a nice return on this first-phase investment. The parking garage is an important competitive amenity for our casino. We further believe that the Imperial Hotel and Casino can be important contributors to our profitability, particularly since they can be operated as adjuncts to the neighboring Bronco Billy's. Hence, we can operate them without incurring additional overhead costs.

Most importantly, however, the first phase literally creates the site for the larger Bronco Billy's expansion. We are moving quickly, and assuming we receive the City's approval in the next few weeks, we intend to break ground immediately on the parking garage and complete it around year-end. In the meantime, we intend to arrange the financing that will be necessary to build the second phase.

Building a company like Full House is truly a rewarding win-win proposition. We begin by providing creative and fun experiences for our guests. We rely on our employees to help us do this. We work hard to be good employers, providing equitable and stable work environments, opportunities for advancement, and fair and reasonable compensation. We also work hard to fulfill our promises to our lenders, becoming an improving credit over time. In turn, with decreasing amounts of risk, we can obtain funds on favorable terms, allowing us to build new casinos and amenities that provide additional good experiences for our guests and advancement opportunities for our employees. Over time, we build a company. Done properly, it provides solid and favorable returns for our investors. In the end, everyone wins.

I would like to thank our shareholders, lenders, employees and guests for their continued support.

/s/ Daniel R. Lee

Daniel R. Lee

President and Chief Executive Officer

Note: This letter supplants the glossy annual reports that are still prepared by some companies; such a report would not be economical for our small company. For a full description of our financial results, please see our annual report on Form 10-K that was filed with the Securities and Exchange Commission and that is available on our website, at www.fullhouseresorts.com.

This letter contains statements that are "forward-looking statements" within the meaning of the safe harbor provisions of the U.S. Private Securities Litigation Reform Act of 1995. Forward-looking statements are neither historical facts nor assurances of future performance. Some forward-looking statements in this letter include, but are not limited to, the statements regarding Full House's proposed capital improvements and investments at its properties (including the proposed Bronco Billy's expansion and the proposed

Silver Slipper expansion), expected completion timelines and budgets, our operating trends and expected results of operations. Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict and many of which are outside of the control of Full House. Information concerning potential risk factors that could affect Full House's financial condition and results of operations is included in the reports Full House files with the Securities and Exchange Commission, including, but not limited to, its Form 10-K for the most recently ended fiscal year and the Company's other periodic reports filed with the Securities and Exchange Commission. The Company is under no obligation to (and expressly disclaims any such obligation to) update or revise its forward-looking statements as a result of new information, future events or otherwise. Actual results may differ materially from those indicated in the forward- looking statements.

This letter also contains supplemental financial information and should only be viewed in conjunction with our audited financial results reported using U.S. generally accepted accounting principles (GAAP) and as filed with the Securities and Exchange Commission. A reconciliation between non-GAAP measures such as Adjusted EBITDA and Adjusted Property EBITDA and GAAP measures is attached as Annex 1 to this proxy statement and can also be found in the Company's Form 10-K for the fiscal year ended December 31, 2017.

FULL HOUSE RESORTS, INC.

One Summerlin, 1980 Festival Plaza Drive, Suite 680

Las Vegas, Nevada 89135

________________________________________

NOTICE OF ANNUAL MEETING OF STOCKHOLDERS

________________________________________

April 13, 2018

Dear Stockholder:

As I write this letter, it has been just over three years since the board was reconstituted and new management was recruited to lead the company. Since that effort began, our share price has increased from $1.19 on October 8, 2014 to $3.21 at the end of March of 2018.

I view the function of the board as follows: develop a strategy, hire and work with a management team to implement that strategy, allocate capital, measure the results, reward the team or hold them accountable, and plan for the future. My role as chairman is to keep the board focused on these tasks.

To help us with these efforts, we have a wide range of experience in the board room today: legal, human resources, accounting, governance, finance, and a healthy dose of hospitality and gaming.

The board has been fortunate to recruit and work with Dan Lee as the CEO and Lewis Fanger as the CFO. Hopefully, you have met them in person or via teleconference. From day one, Dan and Lewis have reinvigorated the existing team and recruited excellent talent where necessary to improve the company.

The board has worked with management to develop and support a strategy of growing organically where we can and pursuing acquisitions if the price is right. In both instances, we try to generate good returns on our capital.

We have also supported a strategy to strengthen our balance sheet. First, we completed a rights offering in the fall of 2016 to help finance some modest capital projects at each of our properties. Second, we successfully refinanced our first and second lien credit facilities with $100 million of notes in February of 2018. Lastly, we raised approximately $12 million in new equity to continue to fund our growth in March of 2018.

Management and the board own a significant number of shares and we have a substantial amount of our own money at stake. Collectively, we currently beneficially own approximately 16% of the company. I believe that this investment fortifies an owner-oriented culture we hope to promote.

Finally, you are invited to attend our Annual Meeting of Stockholders, which will be held at 10:00 a.m., local time, on May 23, 2018, in the Pioneer Room at Bronco Billy’s Casino and Hotel, located at 233 East Bennett Avenue, Cripple Creek, Colorado 80813.

The following items will be on the agenda:

| |

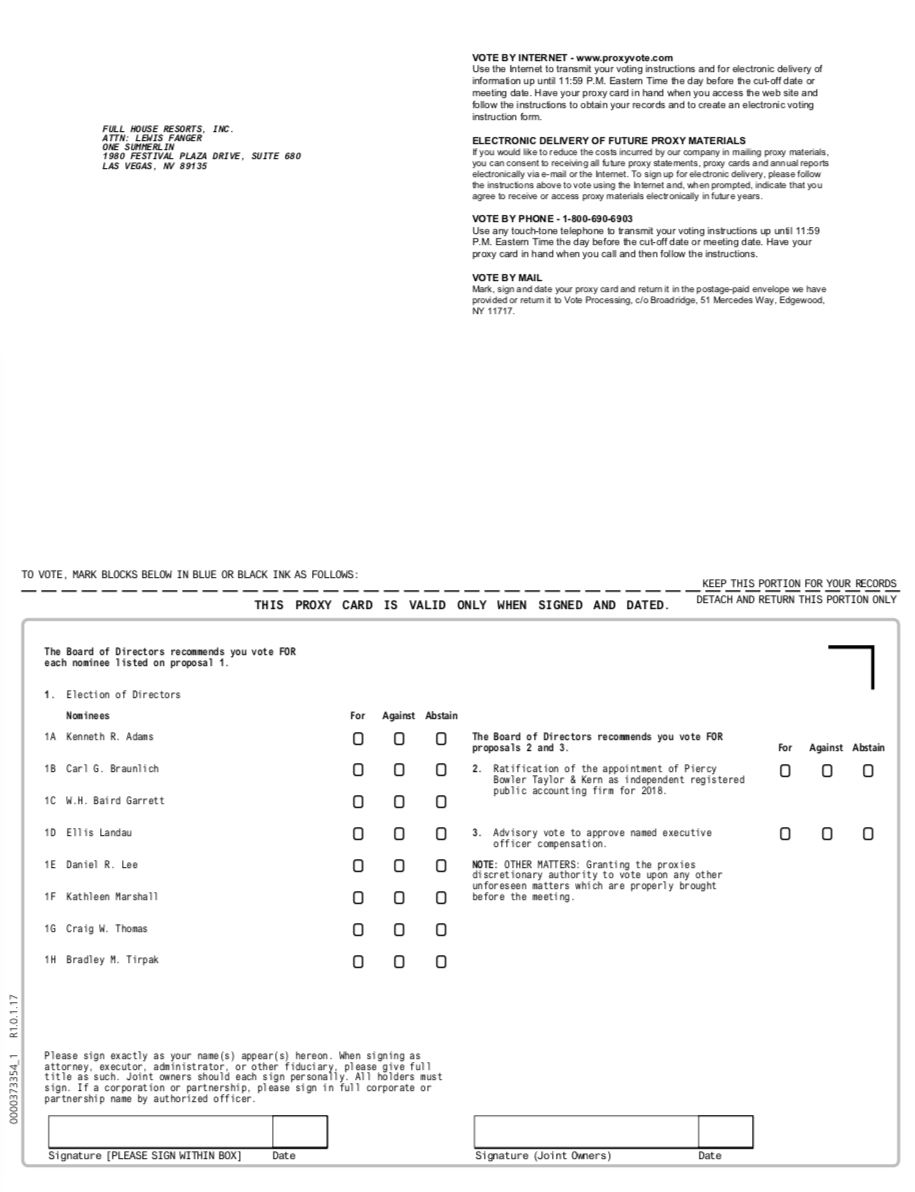

1. | Election of eight members to our board of directors to serve until our next annual meeting of stockholders or until their successors are duly elected and qualified; |

| |

2. | Ratification of the appointment of Piercy Bowler Taylor & Kern, Certified Public Accountants ("Piercy Bowler Taylor & Kern"), as our independent registered public accounting firm for 2018; |

| |

3. | An advisory vote to approve named executive officer compensation; and |

| |

4. | Transaction of such other business as may properly come before the annual meeting, including any adjournments or postponements thereof. |

Our board of directors has fixed the close of business on April 5, 2018 as the record date for determining those stockholders entitled to notice of, and to vote at, the annual meeting and any adjournments or postponements thereof.

I look forward to seeing you at the meeting. If you are unable to attend, I would still welcome your feedback. I am always available.

Sincerely,

/s/ Bradley M. Tirpak

Bradley M. Tirpak

Chairman

This proxy statement, including the form of proxy, the letter from our President and Chief Executive Officer, and our 2017 Annual Report are first being mailed to stockholders on or about April 13, 2018.

________________________________________

TABLE OF CONTENTS

________________________________________

________________________________________

PROXY STATEMENT

________________________________________

This proxy statement contains information relating to the 2018 Annual Meeting of Stockholders of Full House Resorts, Inc. (referred to herein as “we”, “us”, “our” and the “Company”), to be held at 10:00 a.m., local time, on May 23, 2018, in the Pioneer Room at Bronco Billy's Casino and Hotel, located at 233 East Bennett Avenue, Cripple Creek, Colorado 80813, and to any adjournments or postponements.

IMPORTANT NOTICE REGARDING THE AVAILABILITY OF PROXY MATERIALS FOR

THE STOCKHOLDER MEETING TO BE HELD ON MAY 23, 2018

This proxy statement, form of proxy and our annual report on Form 10-K are also available on our website at www.fullhouseresorts.com or at www.proxyvote.com.

________________________________________

ABOUT THE MEETING

________________________________________

What is the purpose of the annual meeting?

At the annual meeting, stockholders will act upon the matters outlined in the accompanying notice of meeting, including:

| |

• | the election of eight directors; |

| |

• | the ratification of Piercy Bowler Taylor & Kern as our independent registered public accounting firm; and |

| |

• | an advisory vote to approve named executive officer compensation. |

The stockholders also will transact any other business that properly comes before the meeting.

Who is entitled to vote?

Only stockholders of record at the close of business on the record date, April 5, 2018, are entitled to receive notice of the annual meeting and to vote the shares of our common stock that they held on that date at the meeting, or any postponement or adjournment of the meeting. Each outstanding share of common stock entitles its holder to cast one vote on each matter to be voted upon.

What is the difference between a stockholder of record and a beneficial owner?

If your shares are registered directly in your name with our transfer agent, American Stock Transfer & Trust Company, LLC, you are considered the "stockholder of record" with respect to those shares. If your shares are held by a brokerage firm, bank, trustee or other agent ("nominee"), you are considered the "beneficial owner" of shares held in "street name". As the beneficial owner, you have the right to direct your nominee on how to vote your shares by following their instructions for voting included in the enclosed proxy materials.

Who can attend the meeting?

All stockholders as of the record date, or their duly appointed proxies, may attend. Please note that if you are the beneficial owner of shares held in street name, you will need to bring a copy of a brokerage statement reflecting your stock ownership as of the record date. You will also need a photo ID to gain admission.

What constitutes a quorum?

The presence at the meeting, in person or by proxy, of the holders of 40% of the total number of shares of our common stock and preferred stock outstanding on the record date will constitute a quorum, permitting the meeting to conduct its business. As of the

record date, 26,914,259 shares of our common stock were outstanding and held by approximately 89 stockholders of record. As of the record date, no shares of our preferred stock were outstanding. Proxies received but marked as abstentions and broker non-votes will be included in the calculation of the number of shares considered to be present at the meeting for purposes of determining a quorum.

If less than 40% of outstanding shares entitled to vote are represented at the meeting, a majority of the shares present at the meeting may adjourn the meeting to another date, time or place, and notice need not be given of the new date, time or place if the new date, time or place is announced at the meeting before an adjournment is taken.

How do I vote?

If you are a stockholder of record, you may vote:

| |

• | in person at the meeting. |

If you are a beneficial owner of shares held in street name, you must follow the voting procedures of your nominee included in your proxy materials. Beneficial owners who wish to vote in person at the meeting will need to obtain a proxy from their nominee.

If I plan to attend the annual meeting, should I still vote by proxy?

Yes. Casting your vote in advance does not affect your right to attend the annual meeting.

If you vote in advance and also attend the meeting, you do not need to vote again at the meeting unless you want to change your vote. Written ballots will be available at the meeting for stockholders of record.

May I change my vote after I return my proxy card?

Yes. Even after you have submitted your proxy, you may change your vote at any time before the proxy is exercised by filing with our Secretary either a notice of revocation or a duly executed proxy bearing a later date. The powers of the proxy holders will be suspended if you attend the meeting in person and so request, although attendance at the meeting will not by itself revoke a previously granted proxy.

What are the Board’s recommendations?

The enclosed proxy is solicited on behalf of our board of directors (the "Board"). Unless you give other instructions on your proxy card, the persons named as proxy holders on the proxy card will vote in accordance with the recommendations of our Board. The recommendation of our Board for each item in this proxy statement is set forth below:

|

| | | |

Proposal | | Board Recommendation |

1. | To elect eight members to our board of directors to serve until our next annual meeting of stockholders or until their successors are duly elected and qualified. | | FOR each director nominee |

2. | To ratify the appointment of Piercy Bowler Taylor & Kern as our independent registered public accounting firm for 2018. | | FOR |

3. | To approve, on an advisory basis, the named executive officer compensation. | | FOR |

What happens if additional matters are presented at the annual meeting?

Our Board does not know of any other matters that may be brought before the meeting nor does it foresee or have reason to believe that the proxy holders will have to vote for substitute or alternate board nominees. In the event that any other matter should properly come before the meeting or any nominee is not available for election, the proxy holders will vote as recommended by our Board, or if no recommendation is given, in accordance with their best judgment.

What vote is required to approve each item?

|

| | | | | |

Proposal | | Votes Required for Approval | | Abstentions |

1. | Election of directors | | Majority of votes cast | | No impact |

2. | Ratification of Piercy Bowler Taylor & Kern as our auditors | | Majority of votes cast | | No impact |

3. | Advisory vote to approve named executive officer compensation | | Majority of votes cast | | No impact |

For any other item that may properly come before the meeting, the affirmative vote of a majority of the votes cast at the meeting, either in person or by proxy, will be required for approval, unless otherwise required by law.

How are abstentions treated?

Abstentions will not be counted as votes cast in the final tally of votes with regard to any proposal. Therefore, abstentions will have no effect on the outcome of any proposal. As stated above, abstentions will be counted for the purpose of determining whether a quorum is present.

What are "broker non-votes" and how are they treated?

If your shares are held by a broker on your behalf (that is, in "street name"), and you do not instruct the broker as to how to vote these shares on Proposal 1 or Proposal 3, the broker may not exercise discretion to vote for or against those proposals. This would be a "broker non-vote" and these shares will not be counted as having been voted on the applicable proposal. With respect to Proposal 2, the broker may exercise its discretion to vote for or against that proposal in the absence of your instruction. Please instruct your bank or broker so your vote can be counted.

What is the effect of the advisory vote on Proposal 3?

Although the advisory vote on Proposal 3 is non-binding, our Board and its compensation committee will annually review the results of the vote and take them into account in making determinations concerning executive compensation.

Do I have dissenter’s or appraisal rights?

You have no dissenter’s or appraisal rights in connection with any of the proposals described herein.

Where can I find voting results of the annual meeting?

We will announce the results for the proposals voted upon at the annual meeting and publish final detailed voting results in a Form 8-K filed within four business days after the annual meeting.

Who should I call with other questions?

If you have additional questions about this proxy statement or the meeting or would like additional copies of this proxy statement or our annual report, please contact: Full House Resorts, Inc., One Summerlin, 1980 Festival Plaza Drive, Suite 680, Las Vegas, Nevada 89135, Telephone: (702) 221-7800.

________________________________________

PROPOSAL ONE:

ELECTION OF DIRECTORS

________________________________________

Our Amended and Restated By-laws (the "By-laws") provide that the number of directors constituting our Board shall be fixed from time to time by our Board. Our Board currently consists of eight directors. The nominees to be voted on by stockholders at this meeting are Kenneth R. Adams, Carl G. Braunlich, W.H. Baird Garrett, Ellis Landau, Daniel R. Lee, Kathleen Marshall, Craig W. Thomas and Bradley M. Tirpak. Directors are elected by a majority of the votes cast, assuming a quorum is present. The term of office of each director ends at the next annual meeting of stockholders or when his or her successor is elected and qualified.

All nominees have consented to be named and have indicated their intent to serve if elected. We have no reason to believe that any of these nominees are unavailable for election. However, if any of the nominees become unavailable for any reason, the persons named as proxies may vote for the election of such person or persons for such office as our Board may recommend in the place of such nominee or nominees. It is intended that proxies, unless marked to the contrary, will be voted in favor of the election of each of the nominees.

Director Nominees

We believe that each nominee possesses the experience, skills and qualities to fully perform his or her duties as a director and to contribute to our success. In addition, each nominee is being nominated because they each possess high standards of personal integrity, are accomplished in their field, have an understanding of the interests and issues that are important to our stockholders and are able to dedicate sufficient time to fulfilling their obligations as a director.

Each nominee’s biography containing information regarding the individual’s service as a director, business experience, director positions held currently or within the last five years and other pertinent information about the particular experience, qualifications, attributes and skills that led our Board to conclude that such person should serve as a director appears on the following pages.

|

| | | |

| | | |

Kenneth R. Adams | | Mr. Adams is a principal in the gaming consulting firm, Ken Adams Ltd., which he founded in 1990. He is also an editor of the Adams’ Report monthly newsletter, the Adams’ Daily Report electronic newsletter and the Adams Analysis, each of which focuses on the gaming industry. Since 2012, Mr. Adams has been a partner in the Colorado Grande in Cripple Creek, Colorado, a limited-stakes casino with a restaurant and bar. Since August 1997, Mr. Adams has been a partner in Johnny Nolon’s Casino in Cripple Creek, Colorado, also a limited-stakes casino with a restaurant and bar. From 2001 until 2008, he served on the board of directors of Vision Gaming & Technology, Inc., a privately held gaming machine company, and he formerly served on the board of directors of the Downtown Improvement Agency in Reno, Nevada. |

Director | |

Age: 75 | |

Director Since: January 2007 | |

| | |

Committees: | |

● | Audit | |

● | Compliance (Chair) | |

Our Board believes Mr. Adams is qualified to serve as a Director due to his 40 years of gaming industry experience, including specific experience as a casino operator, his knowledge of the casino industry, and his continuing analysis and review of the industry. |

| | | |

|

| | | |

| | | |

Carl G. Braunlich | | Since August 2006, Dr. Braunlich has been an Associate Professor at the University of Nevada, Las Vegas. He holds a Doctor of Business Administration in International Business from United States International University, San Diego, California. Prior to joining the faculty of University of Nevada, Las Vegas, Dr. Braunlich was a Professor of Hotel Management at Purdue University since 1990. Previously, he was on the faculty at United States International University. Dr. Braunlich has held executive positions at the Golden Nugget Hotel and Casino in Atlantic City, New Jersey and at Paradise Island Hotel and Casino, Nassau, Bahamas. He has been a consultant to Wynn Las Vegas, Harrah’s Entertainment, Inc., Showboat Hotel and Casino, Bellagio Resort and Casino, International Game Technology, Inc., Atlantic Lottery Corporation, Nova Scotia Gaming Corporation and the Nevada Council on Problem Gambling. Dr. Braunlich was on the board of directors of the National Council on Problem Gambling, and he has served on several problem gambling committees, including those of the Nevada Resort Association and the American Gaming Association. |

Vice Chairman | |

Age: 65 | |

Director Since: May 2005 | |

| | |

Committees: | |

● | Compensation (Chair) | |

● | Nominating and Corporate Governance | |

● | Compliance | |

| | |

Our Board believes that Dr. Braunlich is qualified to serve as a Director due to his knowledge of and experience gained over 15 years in the casino industry and his position as an educator and consultant to the casino industry. |

| | | |

| | | |

W.H. Baird Garrett | | Since July 2015, Mr. Garrett has served as Senior Vice President of Legal at Elasticsearch, Inc., a leading software company in the enterprise search and data analytics space. From October 2008 through September 2015, Mr. Garrett served as an attorney at VLP Law Group, including as the chair of its Technology Transactions practice group. Mr. Garrett has extensive experience in corporate law, having represented clients as diverse as The Walt Disney Company and the venture capital firm of Kleiner, Perkins, Caufield and Byers. He specializes in the negotiation of complex commercial transactions, particularly those involving new technology and intellectual property, such as the purchase and licensing of gaming devices and online gaming software. Mr. Garrett also previously practiced law at the law firm of Wilson, Sonsini, Goodrich and Rosati in Palo Alto, California and Seattle, Washington. Prior to entering private practice, he clerked for the Delaware Court of Chancery. Mr. Garrett earned a B.A. degree from Pennsylvania State University, an M.A. degree from the University of Chicago and a J.D. degree from the University of Virginia School of Law. |

Director | |

Age: 56 | |

Director Since: November 2014 | |

| | |

Committees: | |

● | Audit | |

● | Nominating and Corporate Governance | |

● | Compliance | |

| | |

Our Board believes that Mr. Garrett is qualified to serve as a Director due to his expertise in complex legal transactions involving technology and gaming devices. |

| | | |

| | | |

Ellis Landau | | Mr. Landau is a private investor who serves on various for-profit and non-profit boards. In 2006, Mr. Landau retired as Executive Vice President and Chief Financial Officer of Boyd Gaming Corporation, a position he held since he joined the company in 1990. Mr. Landau previously worked for Ramada Inc., later known as Aztar Corporation, where he served as Vice President and Treasurer, as well as U-Haul International and the Securities and Exchange Commission. Mr. Landau was President, Treasurer and Director of ALST Casino Holdco, LLC, the holding company of Aliante Gaming, LLC, which owned and operated Aliante Casino + Hotel in North Las Vegas, Nevada until 2016, when the company was sold to Boyd Gaming Corporation. From 2007 to 2011, Mr. Landau was a member of the board of directors of Pinnacle Entertainment, Inc., a leading gaming company, where he served as chair of the audit committee and as a member of its nominating and governance committee and its compliance committee. Mr. Landau served as a director of Spectrum Group International from 2012 until March 2014. Mr. Landau has served as a director of A-Mark Precious Metals (formerly a part of Spectrum Group International) since March 2014 and is chairman of the audit committee and a member of the compensation committee. Mr. Landau currently holds a gaming license in Indiana and Colorado and he has previously been licensed in Nevada and Mississippi, which are collectively all four of the jurisdictions where we operate. Mr. Landau earned his B.A. in economics from Brandeis University and his M.B.A. in finance from Columbia University Business School. |

Director | |

Age: 74 | |

Director Since: November 2014 | |

| | |

Committees: | |

● | Compensation | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

Our Board believes that Mr. Landau is qualified to serve as a Director due to his knowledge of and experience in the casino and hospitality industries and his experience as a director for gaming companies, as well as his service on various committees of those boards. |

| | | |

|

| | | |

| | | |

Daniel R. Lee | | Mr. Lee was appointed as our President and Chief Executive Officer in November 2014. Mr. Lee was the Managing Partner of Creative Casinos, LLC, a developer of casino resorts, from September 2010 through December 2014. He was previously Chairman and Chief Executive Officer of Pinnacle Entertainment, Inc., a casino operator and developer, from 2002 to 2009. In the 1990s, he was Chief Financial Officer, Treasurer and Senior Vice President of Finance and Development at Mirage Resorts. During the 1980s, Mr. Lee was a securities analyst for Drexel Burnham Lambert and CS First Boston, specializing in the lodging and gaming industries. He serves as an independent director of Associated Capital since November 2015, where he is a member of the governance committee. He also serves as a director of Myers Industries, Inc. since April 2016, where he is a member of the audit committee and the corporate governance and nominating committee. Mr. Lee previously served as an independent director of LICT Corporation and of ICTC Group, Inc. While working as a securities analyst, he was a Chartered Financial Analyst. Mr. Lee earned his M.B.A. and a B.S. degree in Hotel Administration, both from Cornell University. |

Director, President and Chief Executive Officer | |

Age: 61 | |

Director Since: November 2014 | |

| | |

Committees: | |

● | Compliance | |

| | |

| | |

| | |

| | |

Our Board believes that Mr. Lee is qualified to serve as a Director due to his extensive experience in the financial services industry, his experience and knowledge in the gaming, lodging and securities industries and his executive management experience as Chief Executive Officer of a large public corporation. |

|

| | | |

Kathleen M. Marshall | | Ms. Marshall is a Certified Public Accountant who, since March 2017, has served as the Chief Financial Officer of Casino Reinvestment Development Authority (CRDA), a New Jersey State Authority. Previously, she served as the Controller of CRDA from June 2016 to March 2017, and provided consulting services to CRDA from January 2016 to June 2016. From October 2008 through January 2016, Ms. Marshall served as Director of Business Development of Global Connect LLC, a web-based voice messaging company. Prior to that, from July 2003 through August 2008, Ms. Marshall served as Vice President of Finance for Atlantic City Coin & Slot Service Co. Inc., which designs, manufactures and distributes gaming equipment. Between January and June 2003, Ms. Marshall worked as a consultant. From April 1999 to December 2002, she served as Vice President of Finance for the Atlantic City Convention and Visitors Authority, a government agency responsible for enhancing the economy of the region in coordination with the Atlantic City Convention Center. Prior to that, Ms. Marshall held various finance positions with several Atlantic City casinos, including Vice President of Finance at Atlantic City Showboat, Inc. and various internal audit and financial positions at Caesars Atlantic City, Inc. In addition, Ms. Marshall has worked as a public accountant in the audit division of Price Waterhouse.

|

Director | |

Age: 62 | |

Director Since: January 2007 | |

| | |

Committees: | |

● | Audit (Chair) | |

● | Compliance | |

| | |

| | |

| | |

| | |

| | |

Our Board believes that Ms. Marshall is qualified to serve as a Director due to her knowledge of and experience in the casino industry and her background as a financial officer for casino and casino-related companies. |

|

| | | |

Craig W. Thomas | | Mr. Thomas is a professional investor with more than 15 years of investing experience, including as a portfolio manager at CR Intrinsic Investors and S.A.C. Capital Advisors and an analyst at Goff Moore Strategic Partners and Rainwater, Inc. He is currently the co-founder of Shareholder Advocates for Value Enhancement (S.A.V.E.) and manages various other investment partnerships. Prior to becoming a professional investor, Mr. Thomas was a consultant at The Boston Consulting Group. Mr. Thomas is a former director of Laureate Education, Inc. (LAUR) and Direct Insite Corporation, currently Paybox Corp., from May 2011 to June 2014. In addition, Mr. Thomas currently serves as a director of United States Antimony Corporation (UAMY) since May 2016. Mr. Thomas earned an A.B. from Stanford University and an M.B.A. from the Graduate School of Business at Stanford University.

|

Director | |

Age: 43 | |

Director Since: November 2014 | |

| | |

Committees: | |

● | Compensation | |

● | Nominating and Corporate Governance (Chair) | |

Our Board believes that Mr. Thomas is qualified to serve as a Director due to his knowledge and experience in portfolio management, investment analysis and stockholder advocacy. |

|

|

| | | |

| | | |

Bradley M. Tirpak | | Mr. Tirpak is a professional investor with more than 20 years of investing experience. Since 2016, he has served as a portfolio manager and Managing Director at Palm Management UK LP, a private investment company. From 1997 through 2016, Mr. Tirpak was a portfolio manager at Credit Suisse First Boston, Caxton Associates and Sigma Capital Management, and a managing member of various other investment partnerships. Between 1993 and 1996, he was the founder and CEO of Access Telecom, Inc. an international telecommunications company doing business in Mexico. Mr. Tirpak served as a director at Applied Minerals, Inc. from 2015 to 2017 and as a director at USA Technologies, Inc. from 2010 to 2012. He has served as a director at Flowgroup plc since May 2017 and as a director at Birner Dental Management Services, Inc. since 2017, and also currently serves as trustee of The Halo Trust USA. Mr. Tirpak earned a B.S.M.E. from Tufts University and an M.B.A. from Georgetown University.

|

Chairman | |

Age: 48 | |

Director Since: November 2014 | |

| | |

| |

| | |

| | |

| | |

| | |

Our Board believes that Mr. Tirpak is qualified to serve as a Director due to his knowledge and experience as an investor, portfolio manager, and as a stockholder advocate. |

|

|

OUR BOARD RECOMMENDS |

A VOTE “FOR” EACH OF THE NOMINEES. |

________________________________________

CORPORATE GOVERNANCE

________________________________________

Board Leadership Structure

Our Board has not adopted a formal policy regarding the need to separate or combine the offices of Chairman of the Board and Chief Executive Officer. Instead, our Board remains free to make this determination from time to time in a manner that seems most appropriate for us. We currently have separate persons serving as the Chief Executive Officer and as Chairman of the Board, in recognition of the differences between the two roles. Our Chairman is responsible for setting the agenda for each of the meetings of our Board and the annual meetings of stockholders, and our Chief Executive Officer is responsible for our strategic direction and the general management of its business, financial affairs and day-to-day operations. We believe this structure promotes active participation of the independent directors and strengthens the role of our Board in fulfilling both its oversight responsibility and fiduciary duties to our stockholders, while recognizing our day-to-day management direction by the Chief Executive Officer. Accordingly, we believe this structure has been the best governance model for us and our stockholders to date.

Mr. Tirpak currently serves as our Chairman and Dr. Braunlich currently serves as our Vice Chairman of the Board. Mr. Tirpak and Dr. Braunlich are both independent directors. During 2017, the independent directors met two times in conjunction with our regular Board meetings. All of our Board committees are compromised only of independent directors except for our compliance committee, which includes Mr. Lee, our President and Chief Executive Officer. Each committee is chaired by an independent director. Our Board leadership structure is commonly utilized by other public companies in the United States of comparable size and scope. We believe that an independent Chairman and Vice Chairman and only independent directors serving on our Board committees (other than the compliance committee) provide an effective and balanced leadership structure. With experienced and participating independent directors, we believe we have the proper leadership structure.

Independence of Directors

Under the corporate governance standards of the Nasdaq Stock Market LLC ("Nasdaq"), at least a majority of our Board and all of the members of our audit committee, compensation committee, and the nominating and corporate governance committee must meet the test of independence as defined by the listing requirements of Nasdaq. Our Board, in the exercise of its reasonable business judgment, has determined that Mr. Adams, Dr. Braunlich, Ms. Marshall, Mr. Garrett, Mr. Landau, Mr. Thomas and Mr. Tirpak qualify as independent directors, pursuant to Nasdaq and rules and regulations of the Securities and Exchange Commission ("SEC"). In making the determination of independence, our Board undertook a review of director independence, which includes a review of each director’s responses to questionnaires asking about any relationships with us. This review is designed to identify and evaluate any transactions or relationships between a director or any member of his or her immediate family and us, or members of our management or other members of our Board, and all relevant facts and circumstances regarding any such transactions or relationships. In addition, our Board considered the recommendations of our nominating and corporate governance committee, which also considered whether such directors would be deemed to be "independent".

Meetings

During 2017, our Board held eight regular meetings and no special meetings. Each of our directors attended at least 75% of the aggregate of (i) the total number of meetings of the Board that were held during the period in which he or she was a director and (ii) the total number of meetings of all committees on which he or she served that were held during the period in which he or she was a director. We have no specific requirements regarding attendance at the annual meeting of stockholders by our directors. In 2017, all of our directors attended the annual meeting in person.

Board Committees

Our Board has four standing committees: the audit committee, the compensation committee, the nominating and corporate governance committee, and the compliance committee, each of which operates under a written charter adopted by our Board. A current copy of each of the audit committee, compensation committee, compliance committee, and nominating and corporate governance committee charters is available through the Management & Governance-Documents link on our website, www.fullhouseresorts.com. The following table illustrates the current membership of each of our Board’s committees:

|

| | | | | | | | |

Director | | Audit | | Compensation | | Nominating and Corporate Governance | | Compliance |

Kenneth R. Adams | | ● | | | | | | Chair |

Carl G. Braunlich | | | | Chair | | ● | | ● |

W.H. Baird Garrett | | ● | | | | ● | | ● |

Ellis Landau | | | | ● | | | | |

Daniel R. Lee | | | | | | | | ● |

Kathleen M. Marshall | | Chair | | | | | | ● |

Craig W. Thomas | | | | ● | | Chair | | |

Audit Committee

The audit committee is comprised of three members: Ms. Marshall, Mr. Adams and Mr. Garrett. Ms. Marshall serves as chair and financial expert on the audit committee. Our Board has determined that Ms. Marshall is an audit committee financial expert as defined by the rules and regulations of the SEC. Our Board, in its reasonable judgment, has determined that each member of the audit committee is independent, as defined under the applicable Nasdaq listing standards, and meets the enhanced independence standards for audit committee members required by the SEC. Our audit committee held five meetings in 2017.

Among its responsibilities, the audit committee:

| |

• | appoints, compensates, terminates and oversees our independent auditors; |

| |

• | reviews the independent auditor’s proposed audit scope, approach and the independence and the performance of the independent auditors; |

| |

• | reviews and approves our annual internal audit plan; |

| |

• | reviews the adequacy and effectiveness of our system of internal controls over financial reporting and disclosure controls and procedures; |

| |

• | reviews, discusses and approves financial statements and earnings releases prior to filing our periodic reports; |

| |

• | reviews, with management, the management’s discussion and analysis and the audited financial statements and recommends, if appropriate, the inclusion of the audited financial statements in our annual report on Form 10-K; |

| |

• | discusses guidelines and policies to govern risk assessment and risk management; |

| |

• | reviews and approves related party transactions for potential conflicts of interest; and |

| |

• | establishes procedures for receiving, retaining and handling complaints received by us regarding accounting, internal accounting controls, auditing matters or fraudulent financial reporting and for confidential, anonymous submission by employees of related concerns. |

The audit committee also assists our Board in ensuring compliance with legal and regulatory requirements in our financial reporting process.

Please refer to the audit committee report, which is set forth below, for a further description of our audit committee’s responsibilities and its recommendations with respect to our audited consolidated financial statements for the year ended December 31, 2017.

Compensation Committee

The compensation committee is comprised of three members: Dr. Braunlich, Mr. Landau and Mr. Thomas. Dr. Braunlich serves as chair of the compensation committee. Our Board, in its reasonable judgment, has determined that each member of the compensation committee is independent as defined under the applicable Nasdaq listing standards, Rule 16b-3 of the Securities Exchange Act of 1934, as amended (the "Exchange Act") and Section 162(m) of the Internal Revenue Code of 1986, as amended. The compensation committee held four meetings in 2017. The compensation committee is generally responsible for reviewing and making recommendations to our Board regarding all forms of compensation to be provided to our executive officers, directors and, where appropriate, employees.

Among its responsibilities, the compensation committee:

| |

• | reviews and determines the corporate goals and objectives of our chief executive officer, or CEO, and any employee that reports directly to the CEO; |

| |

• | at least annually, evaluates the performance of the CEO and any employee that reports directly to the CEO; |

| |

• | reviews and approves the compensation of the CEO; |

| |

• | reviews and approves, or recommends for Board approval, the compensation of any employee that reports directly to the CEO; |

| |

• | reviews and approves, or recommends for Board approval, individual performance objectives and general compensation goals and guidelines for employees and the criteria by which bonuses to such employees are determined; |

| |

• | reviews and approves, or recommends for Board approval, the compensation policy for executive officers and directors, and such other employees as directed by the Board; |

| |

• | annually reviews and evaluates our incentive compensation plans; and |

| |

• | develops and recommends for Board approval the executive officer succession plan. |

Management provides recommendations to the compensation committee on the amount and type of executive compensation, as well as individual performance objectives for bonuses and incentive compensation, and the compensation committee reviews and considers these recommendations. In formulating its recommendations to the Board, the compensation committee additionally considers our performance as a whole. The compensation committee determines the fulfillment of the individual performance objectives, which are based on specific growth goals consistent with the annual business plan, and recommends individual bonus and incentive compensation amounts to the Board. The compensation committee may delegate its authority to subcommittees or the chair of the committee when it deems appropriate and in our best interest.